It is that time of year again, or maybe even past that time of year, where you are beginning the scramble to put together next year’s budget. You might find it easiest to approach this process by looking at the prior years’ budget or by looking at year-to-date actuals and starting with those numbers. From there, you probably go through each line item estimating slight changes from the prior year. At the end of the day, you arrive at a budget not all that different from the previous.

These approaches are certainly logical, but are you really getting the budget you and your organization need? Have you thought about making a change to this process? I suggest

comparing prior year amounts at the end of the budget planning process rather than the beginning. To illustrate, everything is made easier with tables, so let’s begin there.

In Table 1 you will see the 2019 income statement for Running Wild Inc. and the preliminary 2020 budget. Notice that Running Wild will be starting out with a completely blank budget in the amount columns for 2020. Also notice they are keeping all the same line items, such as marketing expense and facilities expenses, from 2019. They are then adding in a few blank lines for additions and modifications. After setting up your own table, enter the net income at the bottom. Remember your end goal does not always have to leave you in the positive. You may desire to break even or arrive in the negative because you have decided to invest in your organization.

In Table 1 you will see the 2019 income statement for Running Wild Inc. and the preliminary 2020 budget. Notice that Running Wild will be starting out with a completely blank budget in the amount columns for 2020. Also notice they are keeping all the same line items, such as marketing expense and facilities expenses, from 2019. They are then adding in a few blank lines for additions and modifications. After setting up your own table, enter the net income at the bottom. Remember your end goal does not always have to leave you in the positive. You may desire to break even or arrive in the negative because you have decided to invest in your organization.

Next, take a leap. Forget about the net income goal–consider hiding that line altogether. Forgetting about the result will create the budget you want. This initial estimation should be done without considering net income, so it does not affect your initial intuition. If you go through your budget constantly looking back at your outcome, then you are likely to adjust the items you enter towards the bottom of your table. You begin to see yourself as “running out of room” and adjust the numbers closer to the end, rather analyzing the table in its entirety and adjusting items accordingly. We’ve all done it. You are trying to split the pie evenly and as you cut, the pieces become smaller and smaller to ensure there is one for everyone. You want to avoid this and make sure everything gets the appropriately sized piece.

Continue through each line item and fill in the expenses for each column starting with your most important items and the largest budgetary commitments. If you want to spend only $500 on marketing, then do that. Your marketing budget shouldn’t necessarily be affected by what you spent last year. To finish your transformed budget, you need to add up all the revenues and expenses and, in a perfect world, you would arrive at a total of $0. But, let’s face it, that probably didn’t happen. However, no need to worry. If your totals did not equal $0, go back through and adjust any lines in order to get to your zero goal.

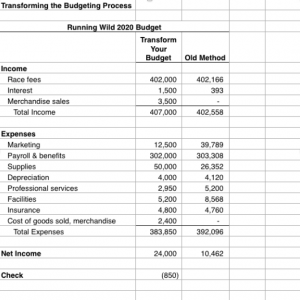

As you are adjusting, remember that not everything needs to appear fixed in your budget just because it has been in the past. There may be ways to reduce seemingly set expenses like rent by negotiating a better lease or by moving to another location. For example, Running Wild has determined through a customer survey that their most common way of attracting new customers is via word of mouth. They removed all print advertising mediums and reduced their social media advertising from two ads a day to one per week in order to focus more on the customer experience. In the normal budgeting process, it may have seemed drastic to cut a marketing budget by $32,000, but when analyzing their marketing needs, it made sense.

There is a time and place for referring back to previous budgets, however. You may want to consider any categories that have drastic changes—5% difference is usually the magic number. These line items may need a little bit of attention before you can just submit your budget. If you have a planned course of action to make these differences a reality, there should be no issue. However, if not, you may want to reconsider your estimates or create steps to make the goal a reality. This will also be important because it is good practice to document all the reasons for significant differences from prior years’ budgets (see “Explanations” column in Table 2). Generally, board members, owners, and management will want to be well informed of the changes.

There is a time and place for referring back to previous budgets, however. You may want to consider any categories that have drastic changes—5% difference is usually the magic number. These line items may need a little bit of attention before you can just submit your budget. If you have a planned course of action to make these differences a reality, there should be no issue. However, if not, you may want to reconsider your estimates or create steps to make the goal a reality. This will also be important because it is good practice to document all the reasons for significant differences from prior years’ budgets (see “Explanations” column in Table 2). Generally, board members, owners, and management will want to be well informed of the changes.

Humans are hardwired so that when we see an initial number—last year’s expenses– we believe that we must remain in that same vicinity in order to stay on track. Generally, this bias prevents us from considering any other information surrounding us. Think about when you are looking to buy a house. You find one you like that is listed for $185,000. However, the majority of people that are going to put in an offer will hope to get a bit of a deal. After all, everyone likes a deal. So you put in an offer for $172,000. For most, this offer is an arbitrary number given without doing a comparative market analysis. What if instead you forgot about the initial asking price, and you looked up comparable home sales in the same zip code. The search finds similar sales of $124,500, $132,000, $119,250 and $122,600. Based on that information it seems like your initial offer was too high a price for that house. $125,000 would be a more reasonable offer and probably the deal you were looking to get. Similar to seeing the price tag on your future home, starting with last year’s numbers will bias the entire process. When you remove this factor from your budgeting process, you can arrive at your ideal plan rather than one created by a previous owner, or even a younger, more naiveté you.

In this table, notice the comparison of budget processes. Running Wild management thought $12,500 for marketing would be perfect to meet all their needs. However, if they had used the old method, Running Wild management may have been hesitant to decrease their marketing budget by $32,000.

In this table, notice the comparison of budget processes. Running Wild management thought $12,500 for marketing would be perfect to meet all their needs. However, if they had used the old method, Running Wild management may have been hesitant to decrease their marketing budget by $32,000.

This can work for a personal budget as well. The table above starts with the end goal of saving $6,000 in your 401(k) and $5,000 in additional savings. It then runs through income and expenses to adjust.